Source > Jacobin

In the age of platform capitalism, everything seems to be changing — except for the well-worn ideological refrains about the disappearance of the working class. The 1990s and 2000s were boom years for the rhetoric of permanent change. Jeremy Rifkin advocated “the end of work” and the Californian ideology of “disruption.” Pundits continually announced the overcoming of class conflict and the restoration of a market society based on consumerist and entrepreneurial citizenship.

This was not just rhetoric, for it was embodied in elements of reality. Underlying this new dominant ideology was the real crisis of Fordism, the model of accumulation that had dominated the postwar period. The declining labour movement, expanding globalization, the birth of the internet, and the financial restoration were accompanied by new forms of accumulation and new paradigms of governance of the capitalist firm and of exchange. The contours of these new paradigms were not defined, but it was clear to most observers that everything was “new” (a “new spirit of capitalism,” according to Luc Boltanski and Ève Chiapello), “post-Fordist,” and “networked” (as Manuel Castells announced in his research). Fordism, with its compromise between capital and labour, its large concentrated and monopolistic companies, and its state interventionism in the economy gave way to the establishment of the free market as a form of regulation of social relations, to the flexible, networked company, concentrated on the core of its activity and outsourcing the rest. In the following decade, the contours of the new post-Fordist paradigm were strengthened with the advent of the platform economy, with Amazon perhaps the most successful example.

Yet the development of Amazon has itself revitalized some of the aspects of Fordism that the new platform capitalism claimed to have overcome: network effects fueled monopoly; venture capital concentrated financial flows; the platform internalized the market within the firm (in their People’s Republic of Walmart, Leigh Phillips and Michal Rozworski showed how Amazon actually resembles a huge, private, economic planning mechanism); and coordination between economic actors has given way to vertical and horizontal integration. Finally, bureaucratized, Taylorized, and massified wage labour has not disappeared, as we see in the recent mobilizations of Amazon workers in the United States and Europe. Rather, logistics operations, the backbone of Amazon’s business, bring together millions of workers around the world. It is from these elements, from this hybridization between platform capitalism and Fordism, that we can identify a specific paradigm: Plat-Fordism.

Parcel Factories

From a business-model point of view, we should start by saying that Amazon has ultimately not invented anything new. Distance selling and large-scale distribution are relatively old phenomena. But Amazon has changed the face of both, hybridizing them. In the 1990s, distance selling and supermarkets were still operating on parallel tracks. Retail had already been a giant of Western capitalism for decades. Walmart opened its first store in 1962, and in the 1990s became the largest US company. As Giovanni Arrighi reminds us in his Adam Smith in Beijing, in 1950 General Motors occupied this position, accounting for 3 per cent of US GDP. Forty years later, Walmart had become the world’s largest employer, with 1.5 million staff and a turnover of 2.3 per cent of US GDP. In 1994, when Jeff Bezos founded Amazon, Walmart’s power seemed out of reach. People talked about Walmart the same way they talk about Amazon today: a giant, the flagship of a new management paradigm. Its opponents denounced its overmighty commercial power and its abuse of workers, proposing its dismantling in the name of antitrust principles. Few people, including Bezos and his well-informed backers, imagined that a home shopping website could rival Walmart in little more than a decade. This was made possible by two things in particular: the financial growth of the technology sector and the logistics revolution.

In the age of platform capitalism, everything seems to be changing — except for the well-worn ideological refrains about the disappearance of the working class.

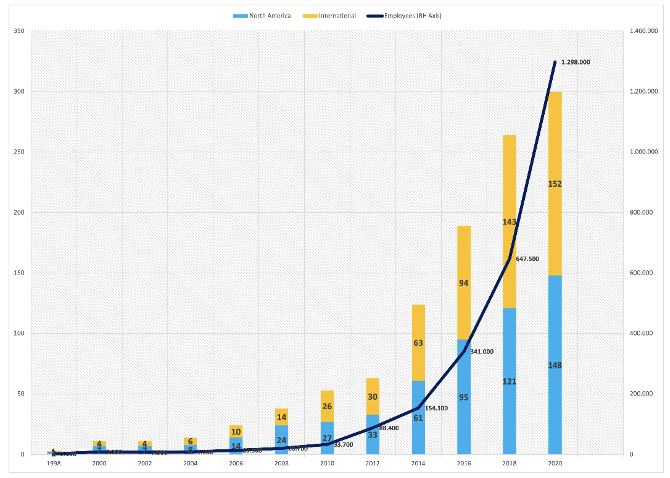

Much has already been said about the logistics revolution, starting with Bruce Allen’s famous article in which the economist predicted a new course in which logistics would evolve from a mere auxiliary function of business organization to a science of managing economic organizations, capable of systemically optimizing transactions, reducing costs, and increasing profits. With the advent of logistics, the “colonization” of what Peter Drucker had already called in 1962 “the last continent of the economy” was to take place — an association that is less metaphorical than it may seem. The facts have proven Allen right. We don’t know if Bezos had read this article, but by 1997, the Amazon founder was already aware of the importance of the logistics network in developing his business. In 1998, Amazon had three large warehouses (called fulfilment centres), and by 2000, it had eleven (seven in North America and four in Europe). The number of employees increased from about two thousand in 1998 to nine thousand in 2000. By 2020, there were over 1.2 million employees and over 300 fulfilment centres.

We don’t know if back then Bezos already had in mind Amazon’s current scale, but the prevailing doctrine of business models recommended just the opposite: a lean, decentralized, outsourced, “networked” structure. Gone were the days of large concentrations of production, of vertical and horizontal integration. The new information technologies, as they used to say in the 1990s, made communication and transactions between the organization and the market more fluid, making it unnecessary to integrate nonessential functions into the company structure.

Moreover, not only were the boundaries of production expanding but also those of markets, thanks to the advent of the internet. Online trade promised a finally decentralized market in which supply and demand would meet online in a transparent economic space without dominant players: only buyers and sellers, the utopia of the transparent, competitive, and meritocratic free market. But this market also needed an infrastructure and someone to take care of it. Soon, companies emerged to provide the virtual infrastructure for the market to match supply and demand, aware also of the promising economic returns that would follow. E-commerce platform eBay has been the most successful, in a first and perhaps decisive step toward the corporatization (commercialization) of the internet. At the same time as experts were celebrating the marriage between the internet and the free market, the market was incorporated into organization: this is how the first platforms were born, with Amazon now occupying a dominant position. But incorporating the virtual market into the organization was only an intermediate step. To win the race of the new e-commerce economy, it was necessary to control not only data flows but also physical ones.

Vertical Integration

Thus, the second and decisive step in Amazon’s path was the marriage between the internet and logistics, between the virtual market and the physical infrastructure. Between the late 1990s and mid-2010s, Amazon built its own logistics network, made up of large fulfilment centres, sorting centres, and delivery stations: an army of employees under its direct control and a fleet of subcontracted deliverers, who were still under its organizational and economic control. Once this stage was completed, Amazon obtained total control of the transactions: their commercial realization (the purchase) and their operational realization (the delivery). For the platform project to be economically viable, one ingredient was needed: economies of scale. Growth would allow Amazon to amortize its infrastructure costs and gain efficiency and better control over the management of physical flows.

The development of Amazon has itself revitalized some of the aspects of Fordism that the new platform capitalism claimed to have overcome.

Amazon’s logistics network was something new compared to traditional supermarket operators and early e-commerce. Unlike the supermarkets, it was not based on a web of local outlets but on large centres from which routes led directly to the customer’s home. This has resulted in a more concentrated network and efficiency gains. But who would set up and run these centres? Unlike before, Amazon wanted to store most of the goods for sale (at the time, this was mainly books) and pick orders directly. This allowed for better process control and, in the intention of Bezos and his associates, a better quality of service.

But it was precisely the unprecedented nature of this hybrid of online and physical retailing that required the organization of work to be designed almost from scratch. It took Amazon several years to adapt the logistics machine to its market strategy. We have gone from “first-generation” warehouses built on the Walmart model — but which proved ill-suited to Amazon’s business — to second-generation warehouses, which are more suitable but also more Taylorized. An example of a second-generation warehouse is the first French centre, which opened in Saran in 2011. Today, with the new semirobotized centres, we have a third-generation model, in which the introduction of Kiva AGV (Automatic Guided Vehicle) robots has considerably increased the productivity of certain segments of the process (even by 300 per cent in picking and 25 per cent in stowing) but at the cost of a further intensification of work rates, as well as an increase in its fragmentation and in IT and managerial control.

Back to Blue Collar

Today, Amazon is the world’s second-largest private employer, with 1.3 million direct employees (in 2020), plus hundreds of thousands of contracted or self-employed drivers. This is essentially a blue-collar workforce. According to my calculations, in Italy in 2020, 88 per cent of employees work in logistics agencies and 5 per cent in customer-service call centres. In 2019, in the subsidiary managing the Italian warehouses, out of 3,516 employees, 3,145 were classified as blue-collar, 270 as white-collar, 91 as middle management, and 11 as management.

Globally, we can only venture estimated numbers. If we count white-collar employees at HQ and at Amazon Web Services (AWS), thus increasing the percentage of skilled labour, we can assume that as many as 70 per cent of employees are warehouse workers or drivers. These figures change the landscape of a sector such as commerce, which with Amazon has undergone an accelerated process of industrialization or if you like, “logisticization.” The concentration and centralization of labour and capital have continued the long-standing trends initiated by mass retailing but have been reinforced by computerization and an unprecedented level of leverage. This has been made possible by the pursuit of a partially unorthodox line of development from the dominant models of the 1990s and 2000s.

Industrial relations have also changed across the different phases of Amazon’s development: progressive Taylorization and partial robotization have increased control over the workforce, which has limited monetary incentives and the variable part of the wage (which were earlier important). In 2018, in the United States, faced with a tight labour market and thanks to pressure from the political and trade union left, Amazon raised the entry-level wage to $15 per hour. At the same time, productivity bonuses and the share-distribution program were cancelled while the stock’s value continued to rise. This attracted a new workforce and penalized older workers, which we might speculate (for want of accessible data) encouraged staff turnover.

As Amazon grew, it found ever greater resistance at the union level and in the workplaces: first in Europe, where a first cycle of struggle affected Germany (2013), France (2014), Poland (2015), Italy (2017), and Spain (2018) and allowed unions to gain a stable foothold; then, a second cycle of mobilizations, during the pandemic, began in the United States, resumed in France and Italy, and has not yet stopped. In the US, it led to a first organizing campaign spearheaded by the Retail, Wholesale and Department Store Union (RWDSU) in Bessemer, Alabama, but it was defeated in January 2021. However, success came very recently, in April 2022, when the Amazon Labor Union won a referendum at a Staten Island site. In France presently, a rolling strike is underway across all Amazon warehouses to demand a wage increase and better working conditions, while in Italy the unions have announced a mobilization over working hours.

Amazon has to acknowledge the existence of a potential counterpower in the heart of its logistics machine.

If ten years ago, Amazon, with its modernizing iconography, consumerist ideology, and anti-union culture, mixing Walmart-style neopaternalism with the new spirit of Silicon Valley, appeared to be terra incognita for collective workers’ movements, today this image is being challenged, and Amazon has to acknowledge the existence of a potential counterpower in the heart of its logistics machine.

Horizontal Integration and Monopolist Rents

Over the years, Amazon’s network has continued to grow not only in logistics but also in other lines of business, notably IT services. 2014 marked a turning point in both dimensions, with the launch of AWS and the opening of the first “last-mile” logistics stations, the penultimate step in a distribution network controlled by Amazon under its own brand. This is no mere coincidence, for these two decisive choices are intrinsically linked. AWS is now publicly acknowledged as Amazon’s “real” strength. Logistics and e-commerce, it is said, are ultimately secondary. In reality, the picture is more complex: first, because it is not sufficiently emphasized how AWS originates from Amazon’s logistics business. To build and manage its physical infrastructure, Amazon also had to build an IT infrastructure. In the days of the first-generation warehouses, it relied on external suppliers. Bezos tells us how it happened, in his 2010 letter to shareholders:

State management is the heart of any system that needs to grow to very large size. Many years ago, Amazon’s requirements reached a point where many of our systems could no longer be served by any commercial solution: our key data services store many petabytes of data and handle millions of requests per second. To meet these demanding and unusual requirements, we’ve developed several alternative, purpose-built persistence solutions, including our own key-value store and single table store. To do so, we’ve leaned heavily on the core principles from the distributed systems and database research communities and invented from there. The storage systems we’ve pioneered demonstrate extreme scalability while maintaining tight control over performance, availability, and cost. To achieve their ultra-scale properties these systems take a novel approach to data update management: by relaxing the synchronization requirements of updates that need to be disseminated to large numbers of replicas, these systems are able to survive under the harshest performance and availability conditions. These implementations are based on the concept of eventual consistency. The advances in data management developed by Amazon engineers have been the starting point for the architectures underneath the cloud storage and data management services offered by Amazon Web Services (AWS). For example, our Simple Storage Service, Elastic Block Store, and SimpleDB all derive their basic architecture from unique Amazon technologies.

In the words of a former Amazon engineer I interviewed, “Amazon is a technology company, but its warehouses are a huge laboratory where we develop new technologies to sell to third parties.” (Think of the partnerships with Volkswagen, John Deere, or the US government itself, and even more recently with Stellantis.) Logistics becomes a service to sell to other companies, large and small. While building its own distribution network, Amazon could also establish its service for third-party sellers (FBA, Fulfillment-by-Amazon). Independent sellers can present their products on Amazon’s marketplace and have to pay for this service before they can benefit from Amazon’s well-established distribution system. According to a recent report by the Institute for Local Self-Reliance coled by Stacy Mitchell, which has been documenting Amazon’s monopolistic practices for years, the company extracts more than 30 percent of the value of revenues from third-party sellers.

This “tax” on external vendors is said to account for 23 per cent of Amazon’s total revenue (including AWS). In contrast, AWS revenues account for “only” 12 per cent.

As Forbes recently put it, “The marketplace for third-party sellers is Amazon’s golden goose, not AWS.” Amazon’s expansion has thus been vertical, with the completion of its logistics network, and horizontal, with the development of new business lines, mostly spin-offs of its logistics operations, all integrated with each other.

In and Out of Finance

This accelerated growth has taken place in a constant interweaving with finance. With its IPO in 1997, Amazon raised an initial $500 million in financing. In subsequent years, thanks to its CFO Joy Covey, Amazon was one of the first companies in the new economy to raise debt financing: $2.25 billion in March 2000, allowing it to survive the bursting of the bubble. The first few years after listing were the most complicated both operationally (logistics struggled to take off) and financially (Amazon piled up loss after loss and did not offer dividends or short-term gains). Bezos and the other executives were clear, bordering on arrogance: what matters is the long term. This was indeed a choice against the prevailing financial ideology that recommended short-term profits and dividends. Yet if profitability was low or nil, other fundamentals were encouraging: turnover was up, as was cash flow. It must also be said that at certain key moments, Amazon realigned itself with “short-termist” Wall Street doxa. In 2000, for example, when its share value was being dragged down by the bursting of the financial bubble, Amazon laid off some 1,300 employees, or 15 per cent of its workforce, in an attempt to improve its accounts.

Once this uncertainty was over, the road was much easier. Since the key period of 2013–14, investor confidence has become certain, and today Amazon’s market value is among the highest on the stock market ($1,700 billion).

The growth in shareholder value has enabled Amazon to fund the expansion of its last-mile logistics, which began around the same time. In turn, the investments increased efficiency and sales, which in turn strengthened the financial strength of the group. Finance and logistics thus entered a virtuous circle. The iconic online retailer eBay shows what happens when these conditions are absent: it never sought to build its logistical backbone and is now worth “only” $42 billion; its turnover in 2020 was around $10 billion, compared to Amazon’s more than $386 billion. eBay did not bet on physical expansion; Amazon did. This allowed it to develop highly profitable (but integrated) secondary business segments: mainly AWS and the FBA service for third parties. The gamble of vertical and horizontal integration — the path an old Fordist company would have followed — has paid off.

True, when we speak of Plat-Fordism, this is no simple return to Fordism. First, the macroeconomic and geopolitical context is much more uncertain and diverse than was perceived in the postwar decades. At the same time, Ford, the company that gave its name to an era, took its first steps in the 1910s to ’20s also in a context of laissez-faire, financial expansion, and geopolitical transition. Second, we cannot ignore the role that new information technologies play in the organization of production nor the importance of digital data nor the centrality of the financial sector. But on top of these elements lies the revitalization of some of the key characteristics of Fordism, precisely where capitalism claimed to have surpassed them. Understanding this reality is key if we are to avoid the ideological traps set by platform capitalism.

The Anti*Capitalist Resistance Editorial Board may not always agree with all of the content we repost but feel it is important to give left voices a platform and develop a space for comradely debate and disagreement.

Art Book Review Books Campism Capitalism China Climate Emergency Conservative Government Conservative Party COVID-19 Creeping Fascism Economics EcoSocialism Elections Europe Event Video Far-Right Fascism Film Film Review Fourth International France Gaza History Imperialism Israel Italy Keir Starmer Labour Party Long Read Marxism Marxist Theory Migrants Palestine pandemic Police Protest Russia Solidarity Statement Trade Unionism Trans*Mission Ukraine United States of America War